The functions sfLogistic(), sfNormal(),

sfExtremeValue(), sfExtremeValue2(), sfCauchy(), and

sfBetaDist() are all 2-parameter spending function families. These

provide increased flexibility in some situations where the flexibility of a

one-parameter spending function family is not sufficient. These functions

all allow fitting of two points on a cumulative spending function curve; in

this case, four parameters are specified indicating an x and a y coordinate

for each of 2 points. Normally each of these functions will be passed to

gsDesign() in the parameter sfu for the upper bound or

sfl for the lower bound to specify a spending function family for a

design. In this case, the user does not need to know the calling sequence.

The calling sequence is useful, however, when the user wishes to plot a

spending function as demonstrated in the examples; note, however, that an

automatic \(\alpha\)- and \(\beta\)-spending function plot

is also available.

sfBetaDist(alpha,t,param) is simply alpha times the incomplete

beta cumulative distribution function with parameters \(a\) and \(b\)

passed in param evaluated at values passed in t.

The other spending functions take the form $$f(t;\alpha,a,b)=\alpha

F(a+bF^{-1}(t))$$ where \(F()\) is a

cumulative distribution function with values \(> 0\) on the real line

(logistic for sfLogistic(), normal for sfNormal(), extreme

value for sfExtremeValue() and Cauchy for sfCauchy()) and

\(F^{-1}()\) is its inverse.

For the logistic spending function this simplifies to $$f(t;\alpha,a,b)=\alpha (1-(1+e^a(t/(1-t))^b)^{-1}).$$

For the extreme value distribution with $$F(x)=\exp(-\exp(-x))$$ this

simplifies to $$f(t;\alpha,a,b)=\alpha \exp(-e^a (-\ln t)^b).$$ Since the

extreme value distribution is not symmetric, there is also a version where

the standard distribution is flipped about 0. This is reflected in

sfExtremeValue2() where $$F(x)=1-\exp(-\exp(x)).$$

Usage

sfLogistic(alpha, t, param)

sfBetaDist(alpha, t, param)

sfCauchy(alpha, t, param)

sfExtremeValue(alpha, t, param)

sfExtremeValue2(alpha, t, param)

sfNormal(alpha, t, param)Arguments

- alpha

Real value \(> 0\) and no more than 1. Normally,

alpha=0.025for one-sided Type I error specification oralpha=0.1for Type II error specification. However, this could be set to 1 if for descriptive purposes you wish to see the proportion of spending as a function of the proportion of sample size or information.- t

A vector of points with increasing values from 0 to 1, inclusive. Values of the proportion of sample size or information for which the spending function will be computed.

- param

In the two-parameter specification,

sfBetaDist()requires 2 positive values, whilesfLogistic(),sfNormal(),sfExtremeValue(),sfExtremeValue2()andsfCauchy()require the first parameter to be any real value and the second to be a positive value. The four parameter specification isc(t1,t2,u1,u2)where the objective is thatsf(t1)=alpha*u1andsf(t2)=alpha*u2. In this parameterization, all four values must be between 0 and 1 andt1 < t2,u1 < u2.

Value

An object of type spendfn.

See vignette("SpendingFunctionOverview") for further details.

Note

The gsDesign technical manual is available at https://keaven.github.io/gsd-tech-manual/.

References

Jennison C and Turnbull BW (2000), Group Sequential Methods with Applications to Clinical Trials. Boca Raton: Chapman and Hall.

Author

Keaven Anderson keaven_anderson@merck.com

Examples

library(ggplot2)

# design a 4-analysis trial using a Kim-DeMets spending function

# for both lower and upper bounds

x <- gsDesign(k = 4, sfu = sfPower, sfupar = 3, sfl = sfPower, sflpar = 1.5)

# print the design

x

#> Asymmetric two-sided group sequential design with

#> 90 % power and 2.5 % Type I Error.

#> Upper bound spending computations assume

#> trial continues if lower bound is crossed.

#>

#> Sample

#> Size ----Lower bounds---- ----Upper bounds-----

#> Analysis Ratio* Z Nominal p Spend+ Z Nominal p Spend++

#> 1 0.282 -0.52 0.3015 0.0125 3.36 0.0004 0.0004

#> 2 0.564 0.53 0.7028 0.0229 2.76 0.0029 0.0027

#> 3 0.846 1.32 0.9072 0.0296 2.36 0.0092 0.0074

#> 4 1.128 2.03 0.9788 0.0350 2.03 0.0212 0.0145

#> Total 0.1000 0.0250

#> + lower bound beta spending (under H1):

#> Kim-DeMets (power) spending function with rho = 1.5.

#> ++ alpha spending:

#> Kim-DeMets (power) spending function with rho = 3.

#> * Sample size ratio compared to fixed design with no interim

#>

#> Boundary crossing probabilities and expected sample size

#> assume any cross stops the trial

#>

#> Upper boundary (power or Type I Error)

#> Analysis

#> Theta 1 2 3 4 Total E{N}

#> 0.0000 0.0004 0.0027 0.0073 0.0116 0.0221 0.579

#> 3.2415 0.0507 0.3248 0.3619 0.1626 0.9000 0.768

#>

#> Lower boundary (futility or Type II Error)

#> Analysis

#> Theta 1 2 3 4 Total

#> 0.0000 0.3015 0.4138 0.2008 0.0619 0.9779

#> 3.2415 0.0125 0.0229 0.0296 0.0350 0.1000

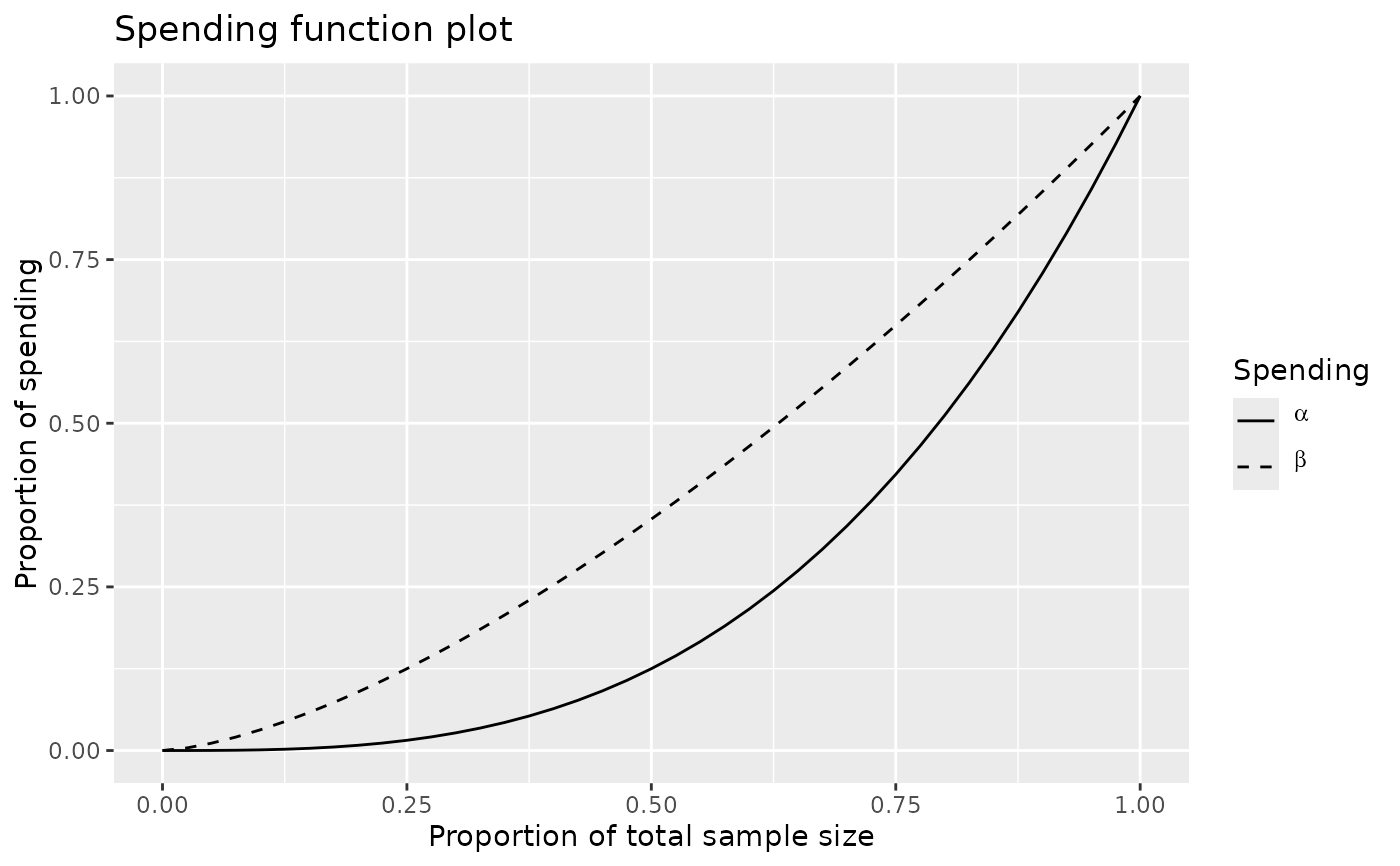

# plot the alpha- and beta-spending functions

plot(x, plottype = 5)

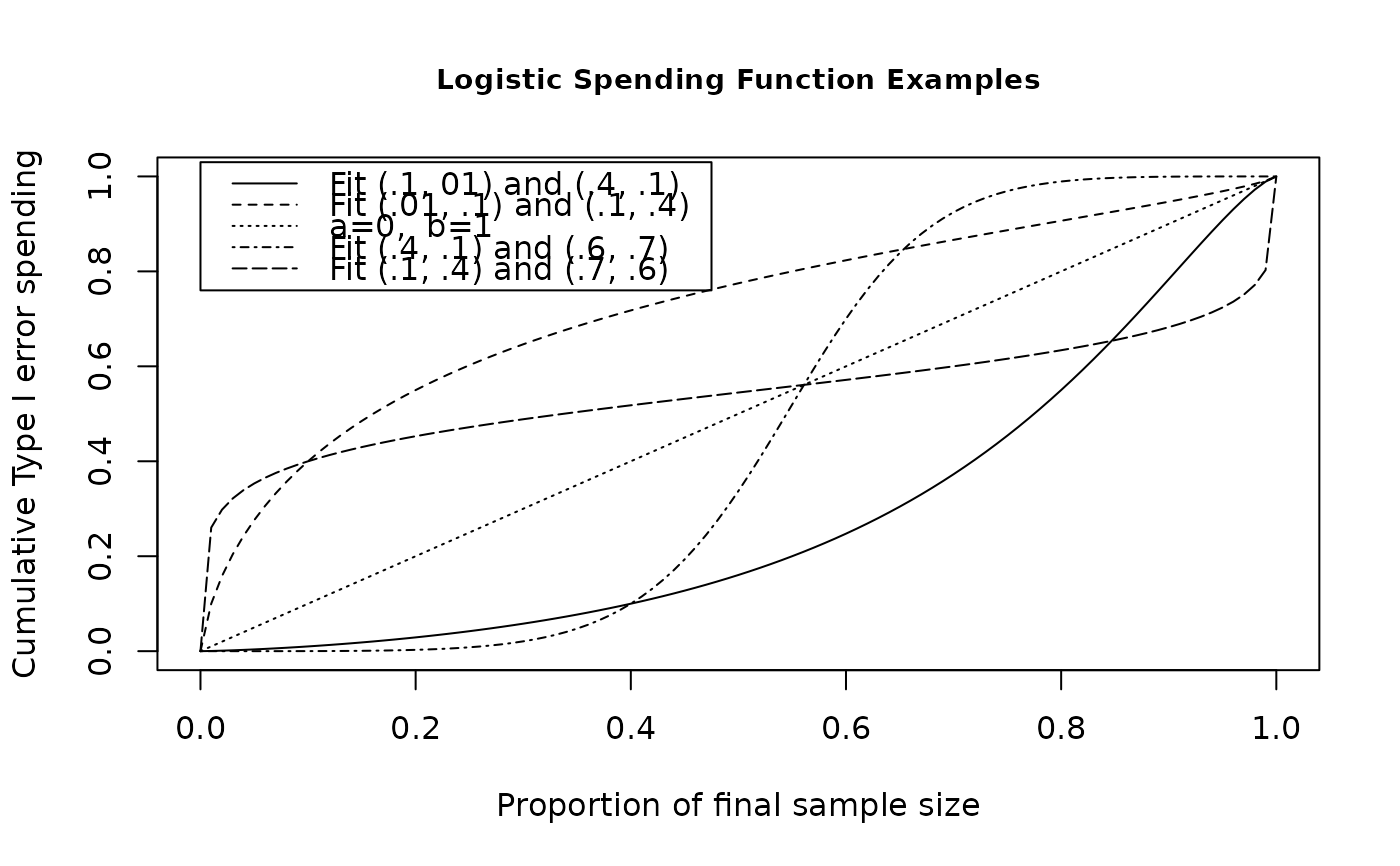

# start by showing how to fit two points with sfLogistic

# plot the spending function using many points to obtain a smooth curve

# note that curve fits the points x=.1, y=.01 and x=.4, y=.1

# specified in the 3rd parameter of sfLogistic

t <- 0:100 / 100

plot(t, sfLogistic(1, t, c(.1, .4, .01, .1))$spend,

xlab = "Proportion of final sample size",

ylab = "Cumulative Type I error spending",

main = "Logistic Spending Function Examples",

type = "l", cex.main = .9

)

lines(t, sfLogistic(1, t, c(.01, .1, .1, .4))$spend, lty = 2)

# now just give a=0 and b=1 as 3rd parameters for sfLogistic

lines(t, sfLogistic(1, t, c(0, 1))$spend, lty = 3)

# try a couple with unconventional shapes again using

# the xy form in the 3rd parameter

lines(t, sfLogistic(1, t, c(.4, .6, .1, .7))$spend, lty = 4)

lines(t, sfLogistic(1, t, c(.1, .7, .4, .6))$spend, lty = 5)

legend(

x = c(.0, .475), y = c(.76, 1.03), lty = 1:5,

legend = c(

"Fit (.1, 01) and (.4, .1)", "Fit (.01, .1) and (.1, .4)",

"a=0, b=1", "Fit (.4, .1) and (.6, .7)",

"Fit (.1, .4) and (.7, .6)"

)

)

# start by showing how to fit two points with sfLogistic

# plot the spending function using many points to obtain a smooth curve

# note that curve fits the points x=.1, y=.01 and x=.4, y=.1

# specified in the 3rd parameter of sfLogistic

t <- 0:100 / 100

plot(t, sfLogistic(1, t, c(.1, .4, .01, .1))$spend,

xlab = "Proportion of final sample size",

ylab = "Cumulative Type I error spending",

main = "Logistic Spending Function Examples",

type = "l", cex.main = .9

)

lines(t, sfLogistic(1, t, c(.01, .1, .1, .4))$spend, lty = 2)

# now just give a=0 and b=1 as 3rd parameters for sfLogistic

lines(t, sfLogistic(1, t, c(0, 1))$spend, lty = 3)

# try a couple with unconventional shapes again using

# the xy form in the 3rd parameter

lines(t, sfLogistic(1, t, c(.4, .6, .1, .7))$spend, lty = 4)

lines(t, sfLogistic(1, t, c(.1, .7, .4, .6))$spend, lty = 5)

legend(

x = c(.0, .475), y = c(.76, 1.03), lty = 1:5,

legend = c(

"Fit (.1, 01) and (.4, .1)", "Fit (.01, .1) and (.1, .4)",

"a=0, b=1", "Fit (.4, .1) and (.6, .7)",

"Fit (.1, .4) and (.7, .6)"

)

)

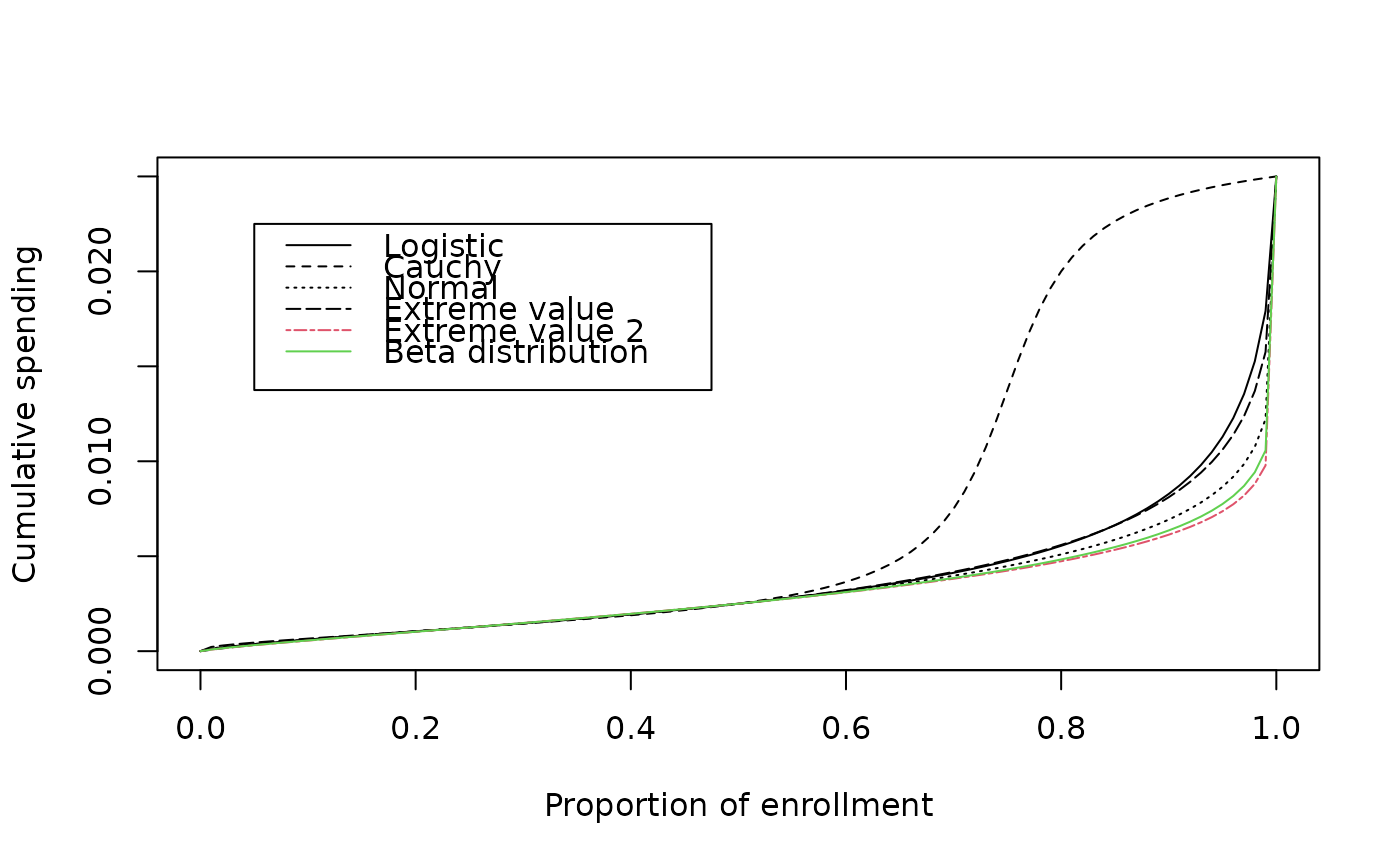

# set up a function to plot comparsons of all

# 2-parameter spending functions

plotsf <- function(alpha, t, param) {

plot(t, sfCauchy(alpha, t, param)$spend,

xlab = "Proportion of enrollment",

ylab = "Cumulative spending", type = "l", lty = 2

)

lines(t, sfExtremeValue(alpha, t, param)$spend, lty = 5)

lines(t, sfLogistic(alpha, t, param)$spend, lty = 1)

lines(t, sfNormal(alpha, t, param)$spend, lty = 3)

lines(t, sfExtremeValue2(alpha, t, param)$spend, lty = 6, col = 2)

lines(t, sfBetaDist(alpha, t, param)$spend, lty = 7, col = 3)

legend(

x = c(.05, .475), y = .025 * c(.55, .9),

lty = c(1, 2, 3, 5, 6, 7),

col = c(1, 1, 1, 1, 2, 3),

legend = c(

"Logistic", "Cauchy", "Normal", "Extreme value",

"Extreme value 2", "Beta distribution"

)

)

}

# do comparison for a design with conservative early spending

# note that Cauchy spending function is quite different

# from the others

param <- c(.25, .5, .05, .1)

plotsf(.025, t, param)

# set up a function to plot comparsons of all

# 2-parameter spending functions

plotsf <- function(alpha, t, param) {

plot(t, sfCauchy(alpha, t, param)$spend,

xlab = "Proportion of enrollment",

ylab = "Cumulative spending", type = "l", lty = 2

)

lines(t, sfExtremeValue(alpha, t, param)$spend, lty = 5)

lines(t, sfLogistic(alpha, t, param)$spend, lty = 1)

lines(t, sfNormal(alpha, t, param)$spend, lty = 3)

lines(t, sfExtremeValue2(alpha, t, param)$spend, lty = 6, col = 2)

lines(t, sfBetaDist(alpha, t, param)$spend, lty = 7, col = 3)

legend(

x = c(.05, .475), y = .025 * c(.55, .9),

lty = c(1, 2, 3, 5, 6, 7),

col = c(1, 1, 1, 1, 2, 3),

legend = c(

"Logistic", "Cauchy", "Normal", "Extreme value",

"Extreme value 2", "Beta distribution"

)

)

}

# do comparison for a design with conservative early spending

# note that Cauchy spending function is quite different

# from the others

param <- c(.25, .5, .05, .1)

plotsf(.025, t, param)