The function sfTDist() provides perhaps the maximum flexibility among

spending functions provided in the gsDesign package. This function

allows fitting of three points on a cumulative spending function curve; in

this case, six parameters are specified indicating an x and a y coordinate

for each of 3 points. Normally this function will be passed to

gsDesign() in the parameter sfu for the upper bound or

sfl for the lower bound to specify a spending function family for a

design. In this case, the user does not need to know the calling sequence.

The calling sequence is useful, however, when the user wishes to plot a

spending function as demonstrated below in examples.

The t-distribution spending function takes the form $$f(t;\alpha)=\alpha

F(a+bF^{-1}(t))$$ where \(F()\) is a cumulative t-distribution function

with df degrees of freedom and \(F^{-1}()\) is its inverse.

Arguments

- alpha

Real value \(> 0\) and no more than 1. Normally,

alpha=0.025for one-sided Type I error specification oralpha=0.1for Type II error specification. However, this could be set to 1 if for descriptive purposes you wish to see the proportion of spending as a function of the proportion of sample size/information.- t

A vector of points with increasing values from 0 to 1, inclusive. Values of the proportion of sample size/information for which the spending function will be computed.

- param

In the three-parameter specification, the first paramater (a) may be any real value, the second (b) any positive value, and the third parameter (df=degrees of freedom) any real value 1 or greater. When

gsDesign()is called with a t-distribution spending function, this is the parameterization printed. The five parameter specification isc(t1,t2,u1,u2,df)where the objective is that the resulting cumulative proportion of spending attrepresented bysf(t)satisfiessf(t1)=alpha*u1,sf(t2)=alpha*u2. The t-distribution used hasdfdegrees of freedom. In this parameterization, all the first four values must be between 0 and 1 andt1 < t2,u1 < u2. The final parameter is any real value of 1 or more. This parameterization can fit any two points satisfying these requirements. The six parameter specification attempts to fit 3 points, but does not have flexibility to fit any three points. In this case, the specification forparamis c(t1,t2,t3,u1,u2,u3) where the objective is thatsf(t1)=alpha*u1,sf(t2)=alpha*u2, andsf(t3)=alpha*u3. See examples to see what happens when points are specified that cannot be fit.

Note

The gsDesign technical manual is available at https://keaven.github.io/gsd-tech-manual/.

References

Jennison C and Turnbull BW (2000), Group Sequential Methods with Applications to Clinical Trials. Boca Raton: Chapman and Hall.

Author

Keaven Anderson keaven_anderson@merck.com

Examples

library(ggplot2)

# 3-parameter specification: a, b, df

sfTDist(1, 1:5 / 6, c(-1, 1.5, 4))$spend

#> [1] 0.02851967 0.08253974 0.18695048 0.38823035 0.72415039

# 5-parameter specification fits 2 points, in this case

# the 1st 2 interims are at 25% and 50% of observations with

# cumulative error spending of 10% and 20%, respectively

# final parameter is df

sfTDist(1, 1:3 / 4, c(.25, .5, .1, .2, 4))$spend

#> [1] 0.1000000 0.2000000 0.3724396

# 6-parameter specification fits 3 points

# Interims are at 25%. 50% and 75% of observations

# with cumulative spending of 10%, 20% and 50%, respectively

# Note: not all 3 point combinations can be fit

sfTDist(1, 1:3 / 4, c(.25, .5, .75, .1, .2, .5))$spend

#> [1] 0.1000000 0.2000000 0.5000006

# Example of error message when the 3-points specified

# in the 6-parameter version cannot be fit

try(sfTDist(1, 1:3 / 4, c(.25, .5, .75, .1, .2, .3))$errmsg)

#> Error in sfTDist(1, 1:3/4, c(0.25, 0.5, 0.75, 0.1, 0.2, 0.3)) :

#> 6-parameter specification of t-distribution spending function did not produce a solution

# sfCauchy (sfTDist with 1 df) and sfNormal (sfTDist with infinite df)

# show the limits of what sfTdist can fit

# for the third point are u3 from 0.344 to 0.6 when t3=0.75

sfNormal(1, 1:3 / 4, c(.25, .5, .1, .2))$spend[3]

#> [1] 0.3439558

sfCauchy(1, 1:3 / 4, c(.25, .5, .1, .2))$spend[3]

#> [1] 0.6

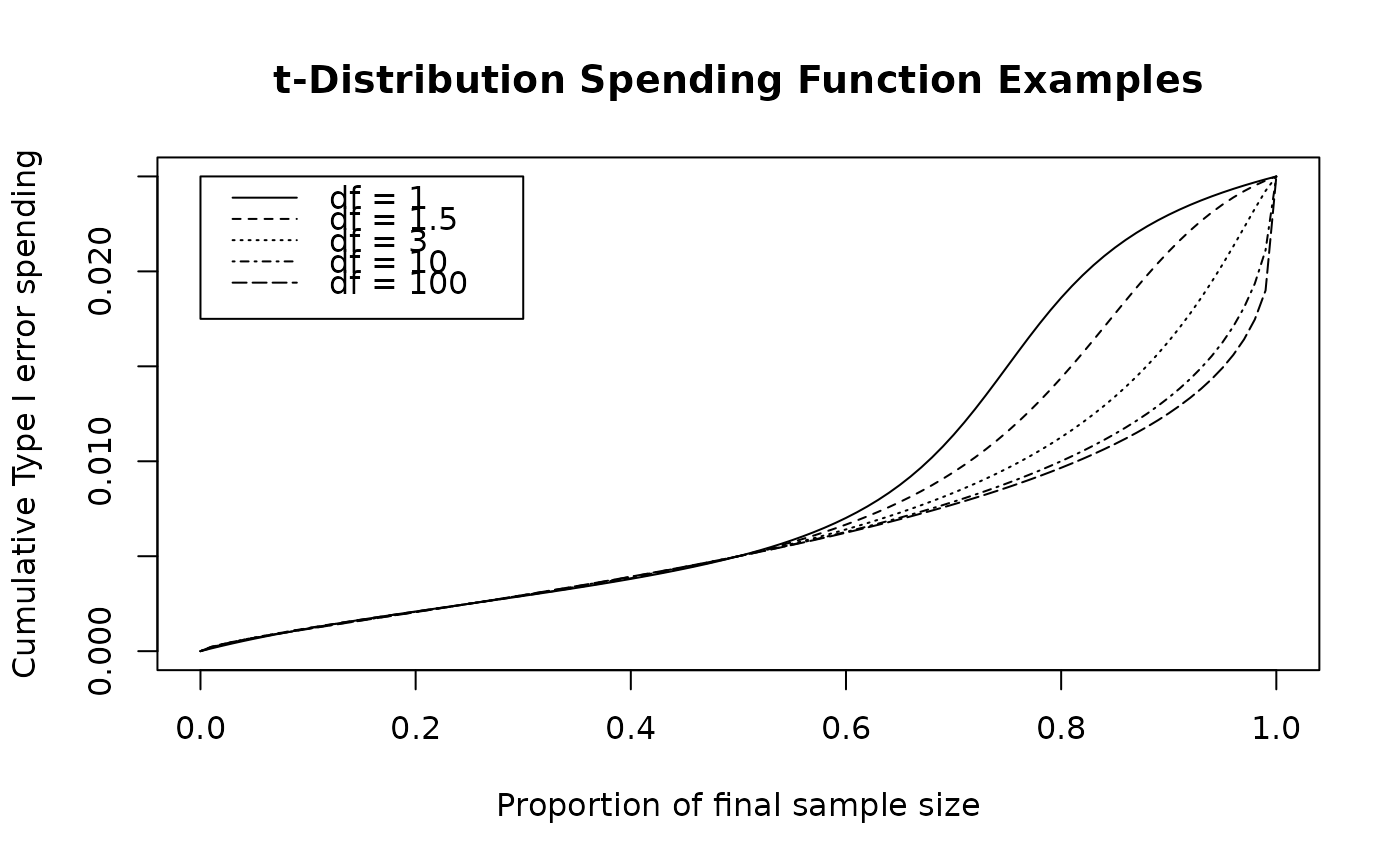

# plot a few t-distribution spending functions fitting

# t=0.25, .5 and u=0.1, 0.2

# to demonstrate the range of flexibility

t <- 0:100 / 100

plot(t, sfTDist(0.025, t, c(.25, .5, .1, .2, 1))$spend,

xlab = "Proportion of final sample size",

ylab = "Cumulative Type I error spending",

main = "t-Distribution Spending Function Examples", type = "l"

)

lines(t, sfTDist(0.025, t, c(.25, .5, .1, .2, 1.5))$spend, lty = 2)

lines(t, sfTDist(0.025, t, c(.25, .5, .1, .2, 3))$spend, lty = 3)

lines(t, sfTDist(0.025, t, c(.25, .5, .1, .2, 10))$spend, lty = 4)

lines(t, sfTDist(0.025, t, c(.25, .5, .1, .2, 100))$spend, lty = 5)

legend(

x = c(.0, .3), y = .025 * c(.7, 1), lty = 1:5,

legend = c("df = 1", "df = 1.5", "df = 3", "df = 10", "df = 100")

)